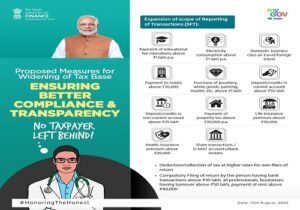

Hotel bill above Rs. 20,000 | Purchase of jewellery, white goods above Rs. 1 lakh will be reported | SFT scope increased

Recently, government has been taking various steps to make things more digital, transparent and inter connected. One step in that direction for changing Form 26AS from normal tax statement to Annual Information statement, sending Compliance notices to tax payers for various issues, discrepancies etc.

When the Form 26AS was updated to Annual Information statement various SFT transactions were included in it to increase the amount of information available in Form 26AS.

Now, while making the announcement about faceless scrutiny, faceless appeal and tax payer charter, our prime minister has increased the scope of Form 26AS/ Annual information statement although same was not mentioned in the speech but it was tweeted by Shri Anurag Thakur (Union minister of State for finance and corporate affairs) on his twitter page.

However, still the same has not been still added to rule 114E where other SFT transactions have been mentioned but soon shall be added and we must be ready for that. So let’s have a look at various transactions added to the list:

| Type of Transaction | Amount (more than) |

| Payment of education fees/ donation | Rs. 1 lakh |

| Electricity consumption | Rs. 1 lakh p.a. |

| Payment to hotels | Rs. 20,000 |

| Purchase of jewellery, white goods, painting, marble etc | Rs. 1 lakh |

| Deposit/ credits in current a/c | Rs. 50 lakh |

| Deposit/ credit in non current a/c | Rs. 25 lakh |

| Payment of property tax | Rs. 20,000 p.a. |

| Life insurance premium | Rs. 50,000 |

| Health insurance premium | Rs. 20,000 |

| Share transaction/ DMAT transaction/ Bank locker | – |

There might be confusion whether details mentioned above are for single transaction or transaction for whole year. It will depend on type of transaction and we also need to wait for Income tax department to include the same in rule 114E where we will get more clarification.

Also many people might think what is included in white goods?

In common parlance white goods mean large electrical goods used domestically such as refrigerators and washing machines, typically white in colour. Thus, this includes all major large electric goods used in house.

Further many people might be thinking that TCS shall be collected on above transaction but that’s not true, the above transactions are just for SFT purpose i.e. information purpose and it will not be chargeable for TCS as of now. SFT is different from TCS.

In addition to above the image published some other information other than SFT which relates to compulsory filing of return of income which is as under:

1. Person having bank transaction above Rs. 30 lakh.

2. Business/ Profession having turnover above Rs. 50 lakh.

3. Payment of rent above Rs. 40,000.

There are a few ambiguities in above condition:

1. Whether they shall be applicable from this Assessment year i.e. 2020-21. Since this have been announced now we think this shall be applicable from next Assessment year i.e. A.Y. 2021-22.

2. Further it has not been clarified whether this rent is for personal house or commercial shop and it is to be assumed that it for per month.

3. Also, a business or profession having turnover of above 50 lakh and saying that they have incurred loss and are not liable to file return won’t be allowed as now one would be required to compulsory file return even if there is a loss if the turnover is above Rs. 50 lakh.

Let’s see when the above changes are incorporated in Income Tax Act.