Individuals, company and trust are receiving notice u/s 143(1)(a) – This is the reason

143(1)(a) is a notice which is issued by CPC, Bangalore the return processing department of CBDT. This notice is issued if any of the following defects is noticed by Income tax department while processing your return:

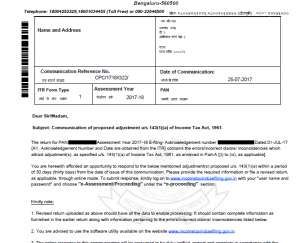

“the total income or loss shall be computed after making the following adjustments, namely:—

(i) any arithmetical error in the return;

(ii) an incorrect claim, if such incorrect claim is apparent from any information in the return;

(iii) disallowance of loss claimed, if return of the previous year for which set off of loss is claimed was furnished beyond the due date specified under sub-section (1) of section 139;

(iv) disallowance of expenditure indicated in the audit report but not taken into account in computing the total income in the return;

(v) disallowance of deduction claimed under sections 10AA, 80-IA, 80-IAB, 80-IB, 80-IC, 80-ID or section 80-IE, if the return is furnished beyond the due date specified under sub-section (1) of section 139; or

(vi) addition of income appearing in Form 26AS or Form 16A or Form 16 which has not been included in computing the total income in the return:”

Thus there are wide number of reasons for which notice u/s 143(1)(a) can be issued and one needs to reply to such notices within 30 days.

However now CPC has started issuing such notices for many wrong reasons where the mistake is on part of processing by CPC and its issuing notice to assessee for a mistake which he has not made.

We had discussed about the same situation in one of our earlier post of capital gain from listed securities.

Now in the second round of processing of return of income CPC is has targeted trust and people earning from speculative business.

In case of trust CPC is issuing notice u/s 143(1)(a) and claiming that the amount of voluntary contribution received for non corpus purpose has been mentioned incorrectly in Part B-TI, and hence making a variance.

Whereas the said column of Part B-TI cannot be filled by assessee and same has been linked to schedule VC in the utility. Hence the argument of department that assessee filling wrong amount in the said schedule is baseless.

Same has been accepted by CPC and when an assessee had a call at customer call center of CPC he was advised that there was a processing error in the back end and he must revise the return and his issue would be resolved.

This is real tax terrorism where assessee and his counsel need to again invest their time to rectify a mistake committed by the department.

This second issue which people are facing is with regard to assessee who had speculative business income and their return are also being processed in same fashion where such speculative business income is being counted twice in business income as was done with capital gain income earlier.

If you go and check the utility of income tax return provided by Income tax department, you’ll come to know that ITR 3, 4, 5, 6 and 7 have been updated from December 2019 to February 2020 on different dates which is way after due date for filing return of income which goes on to prove that there were various mistakes in earlier utility, which has been rectified and now one must get ready to revise their returns for mistakes done by Income tax department.

Do share this post in all the groups so that people can become aware and know that mistake in many cases is on part of department and not assessee. However there can be some cases where mistake might have been done by assessee while filing the return so you must check the notice and ITR available on e filing website to know who has committed the mistake.

If you need assistance you can ask a question to our expert and get the answer within an hour or post a comment about your views on the post and also subscribe to our newsletter for latest weekly updates.